Job-Cost Credit Recording for Returned Electrical Materials

When an electrical supply house issues a credit for returned materials, the contractor must post this credit against the original job number rather than recording it as general miscellaneous income. Accurate credit recording ensures the project's job-cost report reflects the true net material expense. Displaying the true net expense feeds the estimate-versus-actual comparison, which helps the estimating team make tighter, more accurate bids on future projects.

0

1

Tags

Electrical Contracting Business Operations

Running an Electrical Contracting Business Course

Related

Restocking Fee Cost Impact Example

Place the following steps for processing a surplus electrical material return in the correct order.

Match each material return concept in an electrical contracting business with its corresponding outcome or characteristic.

An electrical contractor has surplus materials from a recently completed office renovation: $800 worth of standard receptacles and a $1,500 non-stock, custom-engraved panelboard. The supplier charges a 15% restocking fee on standard returns. What is the correct process the contractor should follow to process the return and maintain accurate project records?

While analyzing the financial recovery from a recently completed project, an electrical contractor forecasts their expected supplier credit by applying a blanket 20% restocking fee deduction to both $600 of standard wire and a $2,000 custom-length bus duct. This financial analysis is correct because distributors will accept returns on any unused project materials as long as the standard restocking fee is paid.

Job-Cost Credit Recording for Returned Electrical Materials

An electrical contractor attempts to return $1,000 in standard breakers and a $500 custom-ordered panelboard to their distributor. The distributor enforces a 20% restocking fee on standard returns and a strict non-returnable policy for custom items. The project manager proposes recording a $1,200 credit against the job number by applying a 20% deduction across the gross purchase amount of all items. You evaluate this financial proposal and reject it as inaccurate because the actual credit mem

You are launching your electrical contracting company and need to draft an internal standard operating procedure (SOP) that your field crews will follow whenever surplus materials remain after completing a job. Which of the following draft procedures best combines all the necessary steps to maximize financial recovery and keep your project records accurate?

Review the provided chart showing a project with a $1,000 material cost and a $200 surplus. Match each specific scenario or document to the correct business action or financial outcome for the project's records.

According to the course content on electrical material returns, what is the typical range for the restocking fee that distributors charge on standard inventory items?

Review the provided chart comparing estimated costs to actual expenses. An electrical contractor completes a project with $1,000 in surplus standard materials. To avoid a 20% supplier restocking fee, the manager decides to move the materials to a different job site rather than returning them and obtaining a credit memo. Evaluate the impact of this decision on the 'Actual' data for the first project. What is the most significant administrative risk of this decision?

An electrical contractor finishes a job with $2,000 in surplus materials: $1,000 in standard stock breakers and $1,000 in custom-length bus duct. The supplier issues an $800 credit memo for the breakers (after a 20% restocking fee) but refuses the return on the bus duct. The project manager suggests recording a $2,000 'internal credit' to the job and moving everything to the warehouse, arguing that the project's financial report shouldn't be penalized for surplus material.

Review the provi

In electrical job costing, if an equipment purchase is not assigned to the correct project or job number, the expense will still appear accurately in that job's cost reports.

Watch the video clip discussing expense transactions. Based on the speaker's explanation, what happens to a project's cost reports if a user fails to select the correct customer project when entering an equipment charge?

As an electrical contractor, applying strict job number discipline is crucial for accurate financial tracking. Match each bookkeeping scenario with the direct consequence it will have on your project cost reports.

Job-Cost Credit Recording for Returned Electrical Materials

As an electrical contractor, you notice a project's profit margin appears falsely high. Arrange the following diagnostic and corrective steps in the logical order to resolve this issue using proper job number discipline.

An electrical contractor is auditing a recently completed project and evaluating why the financial reports show an artificially high profit margin alongside inexplicably high general company overhead. The contractor traces the error to supplier bills and equipment charges that were processed without being assigned to a specific project identifier. To systematically prevent this financial distortion in the future and establish a culture of accountability, the contractor determines they must enfor

You are designing a new 'Field-to-Office' financial protocol for your electrical contracting business to eliminate the problem of 'missing costs' in your project reports. To enforce strict job number discipline, which of the following system architectures should you construct to ensure every material purchase and equipment charge is accurately captured at the source?

To maintain accurate job costing, an electrical contractor must follow a disciplined data-entry process. Arrange the following steps in the correct order to show how a material purchase 'flows' from the supplier into a specific project's financial report.

You are expanding your electrical business and need to architect a new 'Closed-Loop' Job Costing System to ensure that the 'Actual' costs in your financial reports (as shown in the provided summary) are always 100% accurate. To prevent the type of human error where a project selection is nearly missed (as shown in the video clip), which of the following integrated system designs should you construct?

You are reviewing your weekly reports and notice the 'Green Valley Solar' project shows a very high profit margin, but you realize a $450 equipment rental for a trencher is missing from that project's actual costs. You find the charge listed under 'General Overhead' instead. Which action represents the correct application of job number discipline to fix this reporting error?

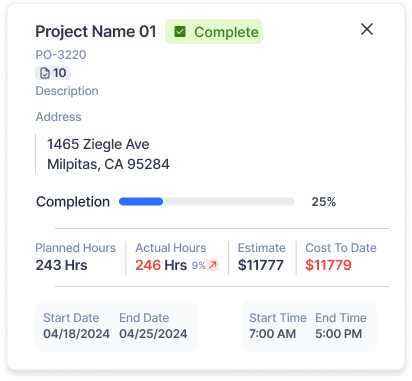

An electrical contractor is reviewing a project's 'Actual vs Estimate' report, similar to the one shown in the image. If the contractor has not maintained strict 'job number discipline' and forgot to assign several material invoices to this specific project, what is the most likely consequence when they interpret this report?

Learn After

When your electrical supply house issues a credit for materials you returned from a completed job, it is acceptable to record that credit as general miscellaneous income for your business rather than posting it against the specific job number.

Match each method of handling leftover electrical materials or supplier return credits with its resulting impact on business job costing and estimating.

After completing a panel upgrade at the Smith residence (Job #402), your lead electrician returns $200 worth of unused breakers to the supply house and receives a credit memo. You are currently purchasing materials for a new basement finish at the Jones residence (Job #403). How should you process this $200 credit in your bookkeeping system to ensure your future estimating remains accurate?

Arrange the following actions in the logical causal sequence that illustrates how properly handling leftover materials translates into improved business operations.

How should an electrical contractor record a credit received from a supply house for returned project materials?

Recording a supply house credit for returned materials as general miscellaneous income, rather than posting it to the original job number, causes the specific project's job-cost report to overstate the true net material expense.

After returning $600 of excess wiring from the 'Oak Street Office' project, an electrical contractor receives a credit from the supply house. To ensure the estimating team has an accurate estimate-versus-actual comparison for future bids, the contractor must post this credit directly against the ________ rather than recording it as general miscellaneous income.

Analyze the causal chain of how properly accounting for excess project materials ultimately improves an electrical contractor's market competitiveness. Arrange the following events in their correct logical sequence.

Evaluate the impact of different administrative and accounting decisions regarding returned materials. Match each action with its corresponding consequence on the electrical contractor's estimating accuracy and job-costing system.

You are designing a 'Data-Driven Bidding' system for your electrical company. Arrange the following steps to construct a complete workflow that ensures material return credits are used to improve the accuracy of your future project proposals.

Referencing the provided 'Actual vs. Estimate' report, your records show 'Actual' material costs of $2,250 for the project. However, you know that $300 worth of excess wiring was returned to the supplier for a credit, but that credit was mistakenly recorded as 'General Miscellaneous Income' instead of being posted to this specific job number. What is the most significant consequence of this error when you analyze this report to prepare for your next bid?

When reviewing an 'Actual vs. Estimate' report like the one shown in the image, what does the 'Actual' material cost column represent if the contractor correctly records credits for returned items?

An electrical contractor's 'Actual vs. Estimate' reports consistently show that 'Actual' material costs match the original purchase orders exactly, even when large amounts of conduit and wire are returned to the supplier. Simultaneously, the company is losing most of its bids to competitors who are pricing jobs 8% lower. By analyzing the relationship between these two facts, what is the most likely structural error in the business's accounting?

You are analyzing an 'Actual vs. Estimate' report (similar to the one shown in the image) for a commercial lighting job. The report displays an 'Estimated' material cost of $8,000 and an 'Actual' material cost of $8,600. You later discover that $1,200 worth of excess fixtures were returned to the supplier for credit, but the office manager recorded this as 'Miscellaneous Income' instead of posting it to the specific job number. What is the true analytical status of this project's material per