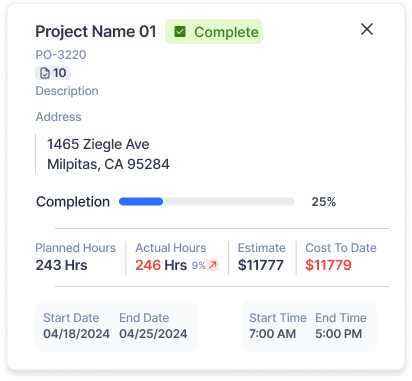

You are analyzing an 'Actual vs. Estimate' report (similar to the one shown in the image) for a commercial lighting job. The report displays an 'Estimated' material cost of $8,000 and an 'Actual' material cost of $8,600. You later discover that $1,200 worth of excess fixtures were returned to the supplier for credit, but the office manager recorded this as 'Miscellaneous Income' instead of posting it to the specific job number. What is the true analytical status of this project's material per

0

1

Tags

Electrical Contracting Business Operations

Running an Electrical Contracting Business Course

Related

When your electrical supply house issues a credit for materials you returned from a completed job, it is acceptable to record that credit as general miscellaneous income for your business rather than posting it against the specific job number.

Match each method of handling leftover electrical materials or supplier return credits with its resulting impact on business job costing and estimating.

After completing a panel upgrade at the Smith residence (Job #402), your lead electrician returns $200 worth of unused breakers to the supply house and receives a credit memo. You are currently purchasing materials for a new basement finish at the Jones residence (Job #403). How should you process this $200 credit in your bookkeeping system to ensure your future estimating remains accurate?

Arrange the following actions in the logical causal sequence that illustrates how properly handling leftover materials translates into improved business operations.

How should an electrical contractor record a credit received from a supply house for returned project materials?

Recording a supply house credit for returned materials as general miscellaneous income, rather than posting it to the original job number, causes the specific project's job-cost report to overstate the true net material expense.

After returning $600 of excess wiring from the 'Oak Street Office' project, an electrical contractor receives a credit from the supply house. To ensure the estimating team has an accurate estimate-versus-actual comparison for future bids, the contractor must post this credit directly against the ________ rather than recording it as general miscellaneous income.

Analyze the causal chain of how properly accounting for excess project materials ultimately improves an electrical contractor's market competitiveness. Arrange the following events in their correct logical sequence.

Evaluate the impact of different administrative and accounting decisions regarding returned materials. Match each action with its corresponding consequence on the electrical contractor's estimating accuracy and job-costing system.

You are designing a 'Data-Driven Bidding' system for your electrical company. Arrange the following steps to construct a complete workflow that ensures material return credits are used to improve the accuracy of your future project proposals.

Referencing the provided 'Actual vs. Estimate' report, your records show 'Actual' material costs of $2,250 for the project. However, you know that $300 worth of excess wiring was returned to the supplier for a credit, but that credit was mistakenly recorded as 'General Miscellaneous Income' instead of being posted to this specific job number. What is the most significant consequence of this error when you analyze this report to prepare for your next bid?

When reviewing an 'Actual vs. Estimate' report like the one shown in the image, what does the 'Actual' material cost column represent if the contractor correctly records credits for returned items?

An electrical contractor's 'Actual vs. Estimate' reports consistently show that 'Actual' material costs match the original purchase orders exactly, even when large amounts of conduit and wire are returned to the supplier. Simultaneously, the company is losing most of its bids to competitors who are pricing jobs 8% lower. By analyzing the relationship between these two facts, what is the most likely structural error in the business's accounting?

You are analyzing an 'Actual vs. Estimate' report (similar to the one shown in the image) for a commercial lighting job. The report displays an 'Estimated' material cost of $8,000 and an 'Actual' material cost of $8,600. You later discover that $1,200 worth of excess fixtures were returned to the supplier for credit, but the office manager recorded this as 'Miscellaneous Income' instead of posting it to the specific job number. What is the true analytical status of this project's material per