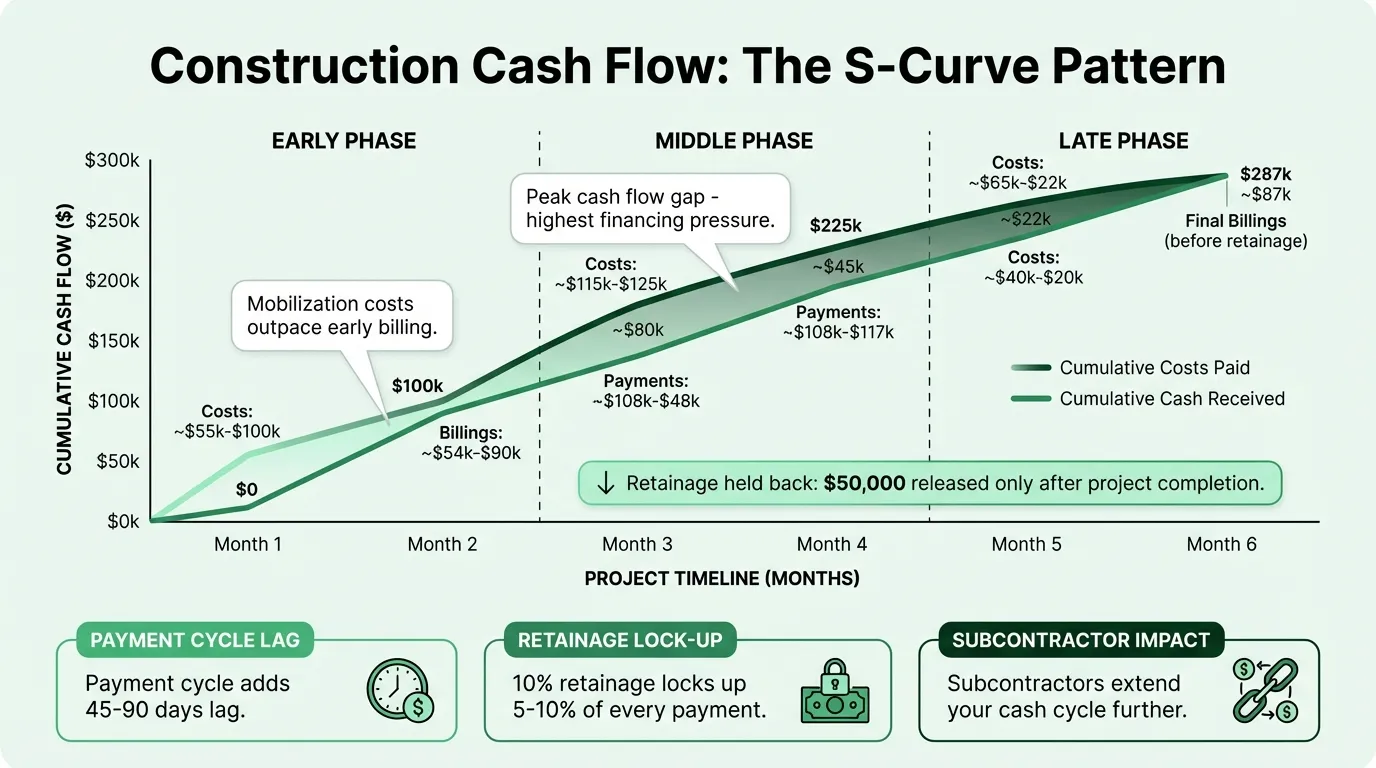

Field and Office Alignment on Percent-Complete Billing

Before the office submits a pay application, superintendents must confirm the percent-complete numbers for every SOV line. When field observations and accounting figures diverge, two risks emerge: under-billing starves cash flow by leaving earned revenue uncollected, while over-billing invites clawbacks or payment holds on future applications. The best pay application is one the field team would defend in a job-site meeting — because they already agreed to the numbers before submission.

0

1

Tags

Electrical Contracting Business Operations

Running an Electrical Contracting Business Course

Related

Field and Office Alignment on Percent-Complete Billing

When submitting an Application for Payment, it is acceptable to bill for unapproved change-order work as long as it appears on a separate line from the original-contract items.

You are an electrical contractor preparing your monthly Application for Payment. You recently finished an approved change order to install additional exterior lighting that was not in the original contract. How should you incorporate this change order into the payment application?

As an electrical contractor preparing your monthly Application for Payment, match each project scenario with how it should be handled on the pay application.

A general contractor requests additional data drops midway through your electrical project. By analyzing the financial risks and auditing requirements, arrange the steps you must take to properly manage and bill for this change order on your Application for Payment.

A general contractor is evaluating an electrical subcontractor's draft Application for Payment and decides to return it for revision. The GC justifies this decision because the subcontractor combined an approved extra work ticket into the main base-scope line item, violating the critical requirement that change-order work must always appear on ________ lines to allow auditors to properly trace the changed scope.

You are designing the billing framework for a new commercial electrical project. To ensure your payment applications are auditable and to prevent disputes regarding base-scope progress, arrange these components in the correct order to construct a professional line-item breakdown.

You are preparing your monthly Application for Payment for a commercial project. You have completed $12,000 of the original contract work. You have also finished $2,000 of work for 'Change Order #1' (signed and approved) and $1,500 of work for 'Change Order #2' (requested by the owner but not yet signed). Which of the following line-item configurations is the correct way to present this to ensure your payment application is not rejected?

You are designing the logic for your electrical business's new automated billing system. To ensure that every Application for Payment generated by the software is audit-ready and protected against rejection, arrange the steps the system must take to properly handle change orders.

Why is it considered a best practice for an electrical contractor to list approved change orders on separate lines of a payment application rather than simply increasing the dollar value of the original contract line items?

A general contractor’s auditor flags an electrical subcontractor’s payment application for 'inflated progress' because the 'Branch Wiring' line item is reported at 110% completion. The subcontractor explains that the extra 10% is for an approved change order that was added to the original line item. Analyzing the auditor's perspective, why did this billing structure lead to a dispute?

Learn After

When an electrical contractor's pay application lists percent-complete figures that are higher than the actual work completed in the field, what is the most likely financial consequence?

When the percent-complete figures listed on a pay application are lower than the work actually finished in the field, the main risk to the electrical contractor is that future pay applications may be subject to clawbacks or payment holds.

Match each percent-complete billing practice with its potential consequence for an electrical contracting business.

You are preparing the monthly pay application for a commercial electrical project. To protect your cash flow and avoid future payment holds, arrange the following steps in the correct order to achieve proper field and office alignment.

If an electrical contractor's office submits a pay application claiming 60% completion on a lighting installation, but the field superintendent confirms that 85% of the work is actually finished, the business is inadvertently starving its own cash flow through the practice of ____.

A project manager preparing a monthly pay application decides to bill a conduit rough-in phase at 85% complete based on the project's original schedule. However, the field superintendent reports that only 60% of the rough-in is actually finished due to recent material delays. The project manager argues that billing at 85% is necessary to maintain positive cash flow and that the field crew can catch up on the work next week. Evaluate the project manager's decision based on the principles of perce

When a superintendent's field observations show a lower percent-complete than the number used on a pay application, the result is called over-billing, which can trigger clawbacks or holds on future payments.

Match each billing scenario with its corresponding consequence or characteristic.

You are establishing a standard operating procedure for your electrical contracting business to prevent cash flow starvation and payment holds. Arrange the following actions in the correct sequence to ensure your pay applications are accurate and defensible.

An electrical contractor is analyzing a project's financials to determine why cash flow is starved, even though the field crew has completed a significant amount of work. They discover that the office submitted the pay application based on outdated, conservative estimates rather than verifying the actual percent-complete with the superintendent. By submitting accounting figures that are lower than actual field observations and leaving earned revenue uncollected, the contractor has inadvertently

Your electrical contracting business is experiencing erratic cash flow. You discover that your office has been facing clawbacks for over-billing on some projects, while simultaneously starving cash flow on other projects by failing to bill for work the field crew has already completed. As the owner, you must design a new Standard Operating Procedure (SOP) to eliminate these discrepancies. Which of the following SOP designs will most effectively align your field and office teams?

Analyze the following discrepancies between the accounting office's cost records and the field superintendent's physical observations for an ongoing electrical project:

- Conduit Installation: Office shows 90% budget spent | Field shows 90% complete

- Panel Upgrades: Office shows 30% budget spent | Field shows 55% complete

- Device Trim-out: Office shows 80% budget spent | Field shows 60% complete

If the office submits a pay application using their own 'budget spent' percenta

An electrical contracting company is struggling with a significant 'Cash Gap' (refer to the provided infographic). The office manager asks the field superintendent to sign a percent-complete report for a pay application that is 15% higher than the actual physical work finished on the job site. The manager argues this is a necessary tactical move to ensure the company can meet its immediate payroll obligations.

Critique the superintendent's decision if he agrees to sign the inflated report to su

In the context of percent-complete billing, what is the primary business risk associated with under-billing?

To ensure that a pay application is accurate and defensible during a job-site meeting, what must the field superintendent confirm before the office submits the document?