Learn Before

Reserve Funding Discipline for Electrical Contractors

Building a reserve requires a repeatable funding habit. Allocate a fixed percentage of every collected payment to a separate reserve account before the money is available for operations. Pair this with the minimum-bank-balance rule: set a floor balance in the operating account and treat it as untouchable for routine spending. A line of credit may serve as a backup layer but should never replace actual liquid reserves, because lenders and surety companies evaluate the contractor's balance sheet—not available credit—when underwriting.

0

1

Tags

Electrical Contracting Business Operations

Running an Electrical Contracting Business Course

Related

Reserve Funding Discipline for Electrical Contractors

When setting a cash reserve target for an electrical contracting business, why must a retainage buffer be added?

Retainage held back on your electrical contracting projects can be counted as available operating cash because it appears as an asset on your books.

Arrange the steps in the correct order to properly integrate a retainage buffer into your contracting business's cash reserves.

You are calculating the cash reserves for your electrical contracting business. Your baseline fixed-cost coverage target is $45,000. Across your active jobs, clients are holding back a typical balance of $15,000 in retainage. To ensure you have enough available cash for operations, your adjusted total cash reserve target must be $____.

As an electrical contractor reviewing your quarterly financials, you must analyze various financial components to accurately determine your cash liquidity. Match each financial scenario with its correct role or impact regarding your adjusted cash reserve target.

An electrical contractor currently covers $40,000 per month in fixed costs and keeps a cash reserve target of $80,000 (two months of fixed costs) plus a $20,000 retainage buffer based on the typical retainage held across active jobs. The contractor just signed a large commercial project that will increase the total retainage balance from $20,000 to approximately $48,000 over the next two months. The contractor decides to leave the reserve target unchanged until the next annual financial rev

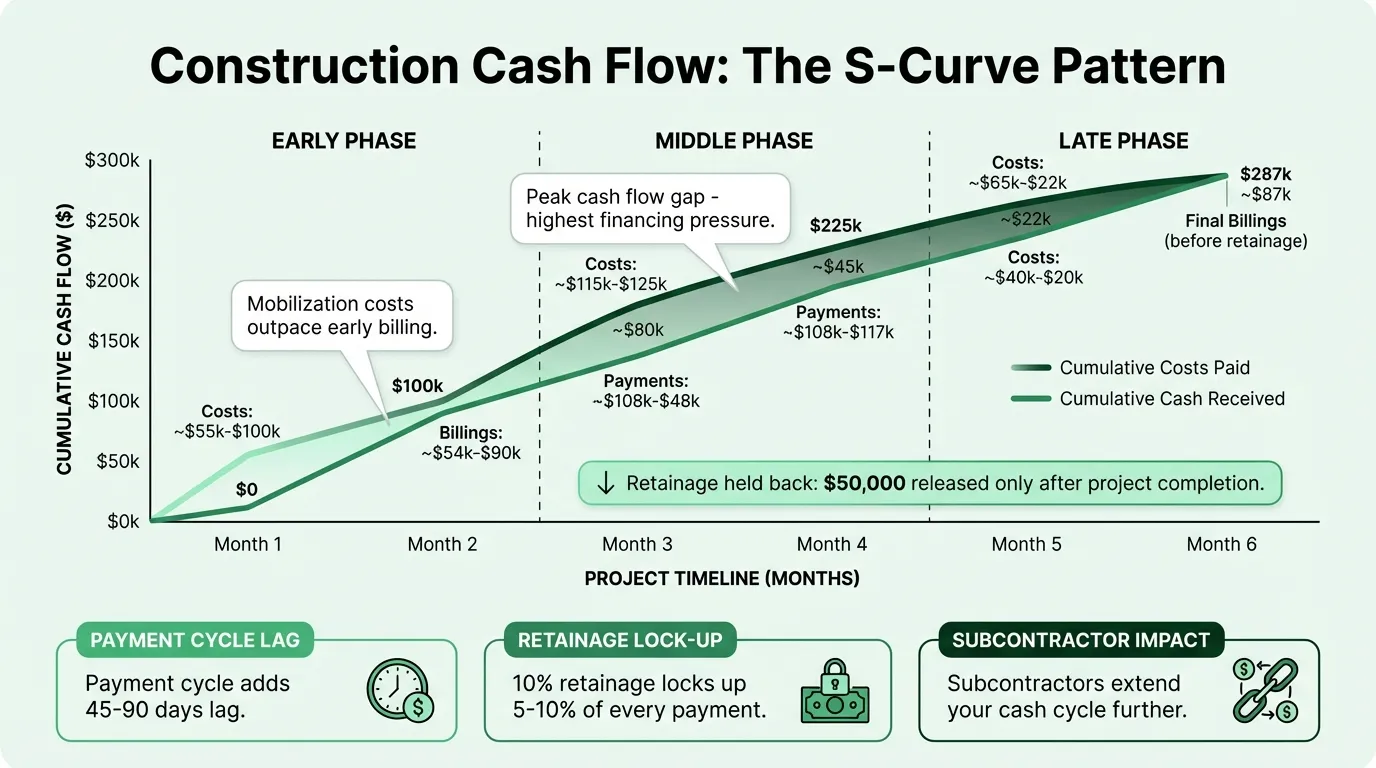

You are tasked with creating a comprehensive 'Cash Reserve Policy' to protect your new electrical business from the liquidity gaps illustrated in the provided infographic. To ensure you always have enough available cash to cover operations despite the 5–10% of billings held back by clients as retainage, which specific model should you design and implement?

An electrical contractor maintains a baseline cash reserve of $40,000 to cover two months of fixed costs. They are evaluating the liquidity needs of two different project portfolios:

Portfolio A: Multiple small residential jobs where 0% is held as retainage. Portfolio B: One large industrial project where $15,000 is currently held back as retainage.

Which statement best analyzes the impact of these portfolios on the contractor's total cash reserve target?

How frequently should an electrical contractor revisit and adjust their retainage buffer to ensure their cash reserve target reflects changes in project sizes and typical retainage percentages?

An electrical contractor is reviewing their business's liquidity. Their current fixed-cost coverage target is $60,000. They have $100,000 in their operating bank account. Their latest quarterly report shows that general contractors are currently holding a total of $50,000 in retainage across all active projects.

The contractor concludes: 'I have $40,000 in surplus cash above my reserve target, so I am in a strong position to start a new high-cost project.'

Using the provided infographic as

Learn After

Current Ratio Benchmark for Contractor Reserve Health

When lenders and surety companies evaluate an electrical contractor for bonding or financing, what do they primarily look at to judge the contractor's financial strength?

Once your electrical contracting business secures a line of credit, it is safe to stop building actual liquid cash reserves because surety companies and lenders view available credit as equivalent to cash on hand.

Match each practical financial scenario to the specific principle of reserve funding discipline it demonstrates for an electrical contracting business.

Analyze the financial workflow required to build a reliable cash reserve. Arrange the following steps in the correct chronological order to demonstrate how an electrical contractor must handle incoming revenue to comply with both the repeatable funding habit and the minimum-bank-balance rule.

You are evaluating the financial stability of an electrical contracting firm that claims its large line of credit eliminates the need to hold cash. You must reject this strategy because surety underwriters judge the firm based on its actual balance sheet; therefore, you should correctly classify their line of credit only as a _____ layer, rather than a replacement for true liquid reserves.

Why shouldn't an electrical contractor use a line of credit to completely replace their actual liquid cash reserves?

Match each financial strategy or concept with its appropriate role in building and maintaining an electrical contractor's cash reserves.

Arrange the following actions in the correct order to demonstrate how an electrical contractor should correctly apply the reserve funding discipline upon collecting a payment from a customer.

An electrical contractor consistently transfers a fixed percentage of every collected payment into a separate reserve account, but routinely spends below their operating account's established floor balance to cover weekly payroll, using a line of credit to bridge the gap. By analyzing this financial behavior, it is accurate to conclude that the contractor is successfully practicing complete reserve funding discipline.

When evaluating the underwriting potential of an electrical contractor who replaced their liquid cash reserves with a large line of credit, you must conclude that their financial strategy is fundamentally flawed. This is because lenders and surety companies base their assessments on the business's actual ____, rather than its available credit.

You are drafting the 'Financial Resilience Protocol' for your new electrical contracting company. Your goal is to architect a system that forces the business to build liquid reserves while protecting daily operations and ensuring you remain eligible for large-project surety bonds. Based on the volatile cash flow cycles illustrated in the infographic, which protocol design correctly synthesizes all the necessary components of reserve funding discipline?

Based on the cash flow volatility illustrated in the infographic, why is an electrical contractor practicing 'reserve funding' advised to treat an operating account floor balance as 'untouchable for routine spending'?

You are designing the 'Financial Integrity Framework' for your new electrical contracting business to withstand the extreme payment cycles shown in the infographic. To build a system that maximizes both your immediate survival and your long-term ability to win large project bonds, match each System Architecture Rule you are implementing to the Financial Vulnerability it is specifically engineered to neutralize.

Looking at the volatile payment cycles in the provided infographic, an electrical contractor decides to maintain their 5% reserve funding habit during a 'dry' period by drawing from their Line of Credit (LOC) to make the transfer. Evaluate the effectiveness of this decision for a contractor whose primary goal is to qualify for a large project surety bond.

Based on the cash flow volatility illustrated in the infographic, an electrical contractor must maintain both a 'fixed percentage' reserve habit and an 'untouchable' floor balance. Analyze why the 'fixed percentage' habit alone is structurally insufficient for protecting the business during the 'dry' periods of negative cash flow.